schools w/ no merit aid

Anonymous

Yeah, life isn't "fair". Someone will always have more than you. Doesn't mean you cannot live an amazing life---it's all about attitude. Plenty of affordable options to get an education |

Anonymous

I do not think you understand very much about economics. Yelling it shouldn't cost so much is silly. I have heard administrative bloat and unnecessary climbing walls as complaints on unnecessary expenses, but someone would have to actually look at what a school is spending money on. The only thing I am certain it is not being spent on are adjunct salaries, but I digress. When a school lowers it tuition, it needs to cut costs. No one is asserting they are making profits, they are by definition non profit entities that I am fairly certain have heavily audited accounts. Maybe there should be limits on how much money families can borrow as an indirect way to limit tuition as schools will adjust to the market. There are limits on how much money students can borrow for undergraduate degrees. Over time, limiting a parents ability to borrow money would make a difference to the extent it limited the number of students that could attend college. Chances are the students hurt by this would not be UMC families but students of families with fewer options for paying for college. This is also pretty paternalistic. |

Anonymous

| OP has a horrible, entitled attitude. How are they JUST realizing private colleges cost $80,000? |

Anonymous

Most do not understand the costs associated with running a university. During Covid, most lost Millions. My own kid's school refunded housing and board for the spring 2020 semester. In the fall they allowed students to take classes remotely and/or live off campus sophomore year (normally it's a 2 year requirement) to de-densify dorms. That meant 30-40% less students in dorms and on a meal plan. Yet the costs associated with providing those services really did not decrease (still have to heat the dorms, clean the bathrooms, etc) . When dorms are empty in the spring 2020, they still had overhead costs associated with it, so they lost a lot of money. Not to mention all the extra costs associated with setting up covid testing, covid quarantine dorms/hotels/extra cleaning/setting up Zoom classroom technology/training professors for zoom teaching/etc. Many schools are still bouncing back from those 2 years of lost income and extra costs. However, fall 2020 the university did NOT increase tuition at all (normally it's 3-5%). They lost 10s of Millions over these 2 years (likely over 100 Million). So either you increase tuition/room&Board or you provide less services for the same costs. Or you run the university into the red and wait to make drastic cuts in the future (not something I want at my kid's university) |

Anonymous

Education is critical yet that doesn't mean that OP's DC will not survive - better yet thrive - at a "less expensive" option (merit + 529). Studies also show that those who can really benefit the most from a T25 education are those who can least afford it. As long as higher ed remains financed as it currently is, then there will be people who need to make decisions based on their budget. You may not like the luxury cars and high-end vacations comparison, but it may be the most apt for a broad range of folks to grasp. |

Anonymous

+100 |

Anonymous

Yes, it doesn't make much sense. Anyone who has made a tiny effort would know that's what the top private colleges would cost in 2022/2023. Our goal was 80K/year for a top university, 50-60K/year for mid level and 30-35K for state---that was what most college calculators have been telling us (along with our financial advisor) since our kids were little. For one kid we planned on 50-60K (smart kid but hates school, has ADHD/processing issues/executive functioning/test taking issues, so we knew early by MS that they would not be targeting universities that cost 80K and not likely to want to continue onto grad school immediately, and if that changed we would be able to cashflow the difference), for the other two we could see them possibly wanting to attend an elite/top university so we saved accordingly-if they go somewhere that costs less then they have some $$ for grad school. However, if we had not been able to save enough, we would have known that by 9th/10th grade and would have worked to develop an appropriate list of colleges to apply to that includes mostly schools we could afford. It's ok to tell your kids you can only afford certain schools, and that while you can apply to the T20 school it's a lottery, you might not get in, and without merit we cannot afford it. Same way you tell your kid they are not getting a brand new sports car for their 16th birthday, despite the fact classmates will get one (my kid's attended a HS where many kids drive 60K sports cars, brand new Teslas---I wouldn't do that for a 16yo even if I could afford it). |

Anonymous

Or, some of us are not taking vacations and living in 1000 fixer uppers in a dcum bad school district to save. |

Anonymous

Plenty of people do that---everyone makes life choices and saves accordingly. That's the point. Someone who has been able to save $160K for education is doing well and they are not "struggling". Plenty of people live in older homes and don't take vacations and still can't save much. |

Anonymous

| I’m always amazed at people who blame “lack of planning” when people don’t have $300K saved for their kid’s education. Some people simply can’t put that much money into a 529 because, wait for it, they simply don’t make enough money to do so. No amount of scrimping, saving, driving beater cars, not taking vacations, will change that. It’s not a character flaw that they don’t have a $300K 529 and I wish people would stop making it sound like it is. |

Anonymous

For families with financial need, there is financial aid. This thread is about merit aid and why many top schools don’t offer it. No one is saying that everyone should have saved $300K for college. What we are saying is that people without financial need are not entitled to a subsidized elite education and that the cost of such education is a surprise to no one paying attention. OP managed to save $160K for college and OP’s student can use that money to get through college debt free and is in better position than many. Do we sympathize that OP cannot afford to send her child to Wellesley with the amount of money she has already saved? No we do not. |

Anonymous

It is not a character flaw. But it would be a character flaw to expect to be able to attend a university that you cannot afford (as in $80K/year) because you were not able to save. There are many, many good universities that do offer merit, that can be affordable to your family. So if you were not able to save and don't qualify for any/enough FA, then an $80K/year school just might not be the "right fit" school for your kids. So like you have done (and most people have to do at some level) with lots of things in life, you pick schools that are affordable to you. There are plenty to pick from. But the reason many mention the "saving" is because we routinely see people complain about not having enough money yet "waste" their money on non-essentials. I see people get a $5 latte daily (sometime two), eat lunch out daily, eat half their dinners out/go to bars, etc yet complain they can't save for something else. So while it won't solve "all the world's problems", those people are wasting $200-800 per month---that could be saved for something else. So if education was more important to them, they could choose to save. It's those people I'm referencing when I make statements like that. When I was younger (and didn't have enough money), I took my lunch 9/10 days, always took coffee and snacks from home, cooked dinner at home most nights, didn't take fancy vacations (ie we took 3-4 day trips that were within a 5-6 hour drive from home and stayed at discount hotels). I grew up poor, so I get that many people simply cannot "just save instead of spending". My family dining out treat when going up was pizza on Sat night or a trip to Ponderosa (steak and all you can eat salad bar for $8/person). However, many, many people I know could save if they wanted to, yet choose to complain about not having everything in life. |

Anonymous

+1000 |

Anonymous

|

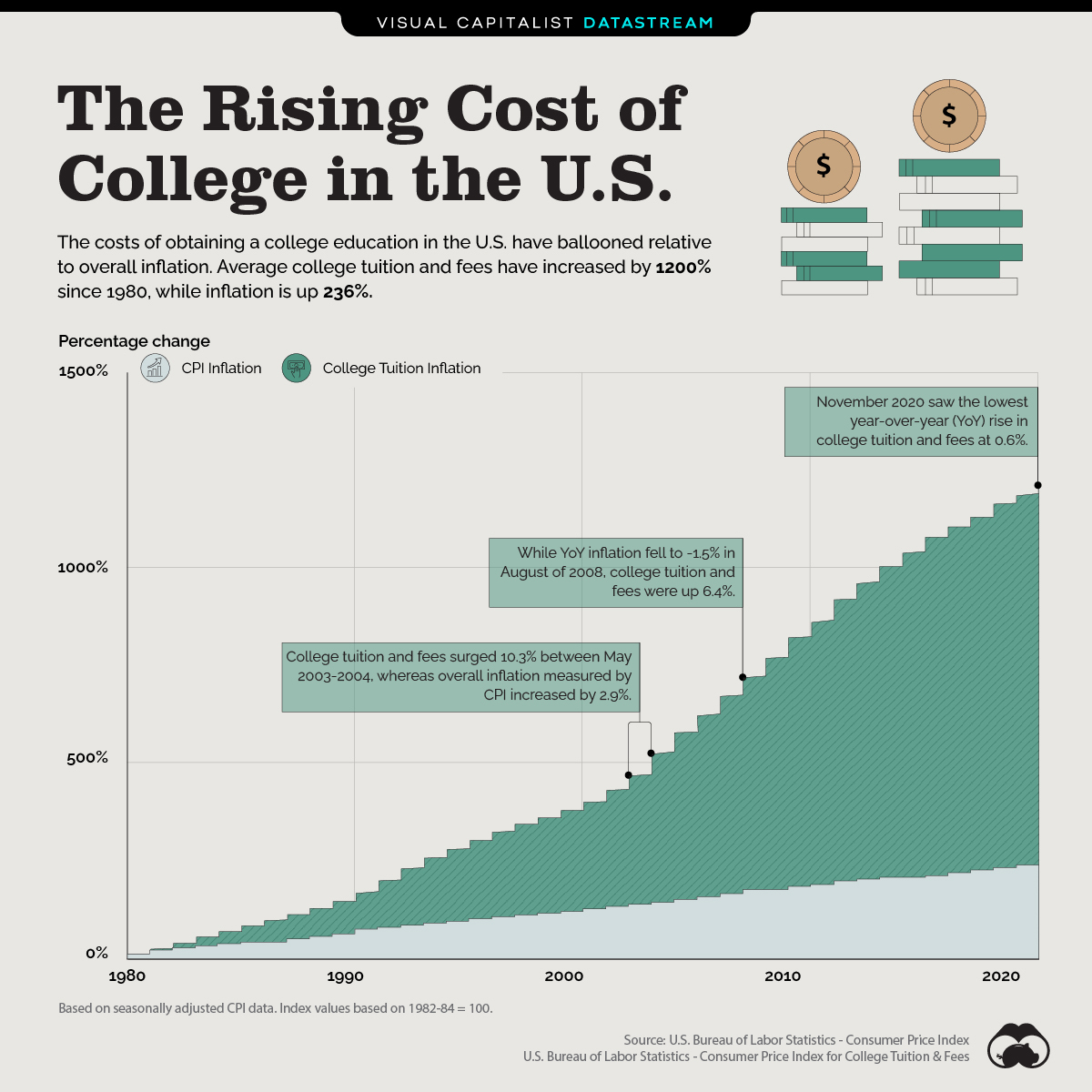

For those of you wondering why tuition has gone up so much--it's not just climbing walls and administrative creep (although that doesn't hurt. Here are some of the things schools must now provide that cost a lot of money:

1) Mental health services 2) ADA and accommodation services (extra test time et al) 3) FERPA/HIIPA administrators 4)DEI deans, programs, counselors, et al 5) Improved housing and dining I'm not saying that these changes are bad--it's great that kids with mental health issues, disabilities, needing accommodations can now go to school, and DEI is important. But if you think about how it was when the boomers went to school -- some large lectures and bare bones housing, no counseling at all -- and what it is like today at schools, you see why it costs so much more. |

Anonymous

|