Federal Reserve: signs abound that housing market is entering bubble territory

Anonymous

| Won't happen. |

Anonymous

The federal reserve literally cited “fear of missing out” as part of the issue. So I guess you think they are idiots? |

Anonymous

I guess they are trying to target the average dumb American who doesn’t understand “irrational exuberance”. Correction <> collapse |

Anonymous

I don't understand why you think people just walk away if their house is underwater, second homes included. If you need a place to live or don't need to sell your second home, you wait it out until the value rises again. It isn't like your home is a checking account where you suddenly have less money to spend. |

Anonymous

First, your (?) constant references to FOMO long predates this article. Second, the Fed points to it as one of numerous factors that may have led to escalating prices. You, on the other hand, in this and previous posts, are certain it is the only cause, and take a perverse delight in deriding it, almost as if you are using your disdain for current buyers to support your belief that you are much smarter than they are. So, short answer, no, I don't think the Fed is comprised of idiots. Just you. |

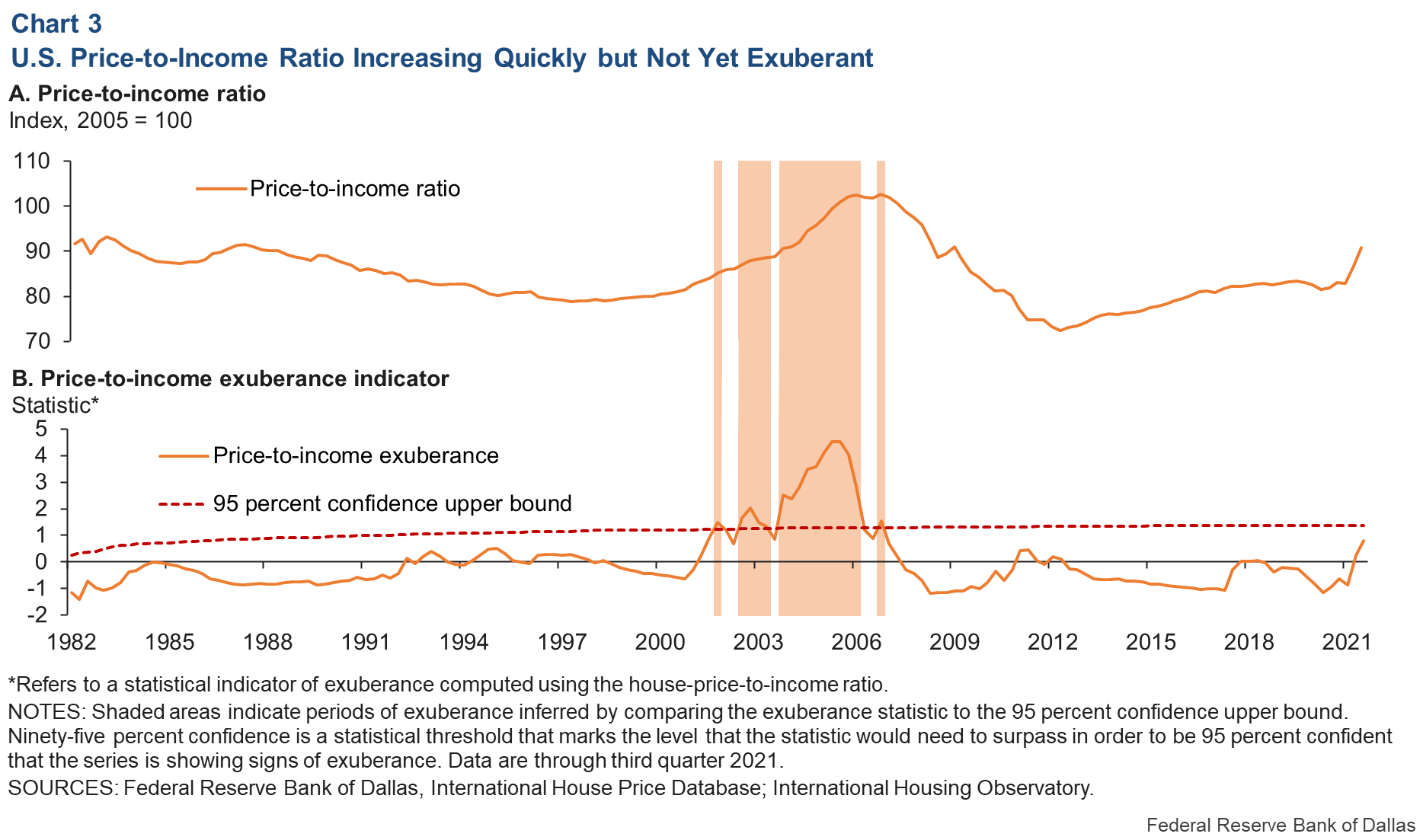

Anonymous

Look at Graph B - House Price Exuberance index.

We are still waaaaaaaaaaaaaaaaaaay below 2003-2007 period. Rising rates will mute price increases for the next few years and keep them largely flat in most of the country. We still have a shortage of homes - particularly for families - in the biggest metro areas (LA, NYC, SF, DC, etc). The cooling of housing prices will not be evenly distributed. I toured a bunch of houses on the Eastern Shore in 2016. Many were still underwater from the housing crisis. One guy was listed $200K under what he paid in 2007 and really wanted to sell so he could move to Florida. He told us that he owned 5 houses in the area and had lost 4 of them in the Crisis. Prices are going to be hit hardest in those areas outside the big metro areas. |

Anonymous

Ask the masses of people who did it last time. Say you bought a vacation home in 2021 for $1.5 million. Suddenly the value is down to $1.1 million. You’re not using it as much as you thought and renting it will not cover then mortgage. Walking away at that point starts to make sense to people. As with the last downturn it can take a loooong time to get back to break even when you buy at the peak. |

Anonymous

Some people can't wait 10-12 years for their house to recover its value. They may have a sickness that prevents them from working. They may be downsized from their government job as the federal government continues to contract its workforce. They may need or want to move for professional or personal reasons (this is especially true in DC, which is a highly transient area). Those people will be underwater on their mortgages if there is a significant correction. You don't need a single dramatic precipitating event to cause people to flood the market trying to get some value out their houses as prices begin to descend. A few underwater properties can affect the entire local market. It's also important to understand that, although a small proportion of buyers in any housing market always end up overextended and get forced into foreclosure, there are many more people overextended in this market right now than is the norm. This is because the combination of (1) pent up desire to move during Covid lockdowns; (2) the increased premium placed on larger homes and outdoor spaces during lockdowns; (3) the incredibly low interest rates, and (4) the feeding frenzy buyers' market this last year all mean that many, many more people over-spent this year (eg spent more than 28% of their salary on their mortgage and/or threw every penny of their available cash into the down payment). As a consequence of these buying behaviors, you would expect to see an increase in the number of foreclosures this year or next, even if housing prices held steady. If prices do not hold steady, then when those more-than-usual number of foreclosures or forced sales hit the market, those sellers will be underwater in their mortgages. Those over-extended forced sales at underwater prices (along with the other kinds of forced sales mentioned above) could potentially cause a housing price cascade. Of course it is difficult to know the timeline for this, but the feeding frenzy has already showed signs of stopping this week. The next step will be price growth slowdown, then growth decline, then price stabilization, then price downturn. How quickly this develops and how dramatically it affects the overall housing market will depend on how much people panic. It could be a small plateau of correction, or it could be a steeper, longer decline. A lot depends on what else is happening with the economy at the same time, and what happens with interest rates. |

Anonymous

People walk away when they don't have any equity in the house because of reduced value, and they can no longer afford to pay the monthly mortgage. Or they don't want to keep paying the mortgage if they can rent for less. If you have no equity in the house, you are not losing anything (other than your credit rating) when you walk away. Read about the 2007-2008 housing crisis. |

Anonymous

You know that all signs indicate that we are heading into a recession, right? In times of recession, businesses contract their workforce, including the federal government. I hope there will not be a recession, but if there is unemployment will rise. |

Anonymous

| I'm confused by everyone referring to the Fed. The Fed has made no such statement. People are referencing an article published by staff at the Federal Reserve Bank of Dallas, a private entity. |

Anonymous

No definition of clickbait necessitates ads. The fact is the headline says "Real-Time Market Monitoring Finds Signs of Brewing U.S. Housing Bubble" and the article says "Based on present evidence, there is no expectation that fallout from a housing correction would be comparable to the 2007–09 Global Financial Crisis in terms of magnitude or macroeconomic gravity. Among other things, household balance sheets appear in better shape, and excessive borrowing doesn’t appear to be fueling the housing market boom." So yeah, it is clickbait. |

Anonymous

| I find it hilarious that people are genuinely arguing over whether an article by Fed economists is "clickbait." Economists at the fed could give a damn whether their article gets clicks. Citations? Oh, yes, that they care about. But whether randos on the internet click on that page? Man, y'all are hilarious. |

Anonymous

Where was the 30% quote? |

Anonymous

Um, no. No, no, no, no. The statements quotes by these various articles were issued by the Federal Reserve Bank of Dallas, which is one of 12 regional banks that (with the Board of Gov in DC) makes up the Federal Reserve. Which is the central bank of the United States. It is not a private entitle. Referring to these statements as issued by the Fed is entirely correct. https://www.bloomberg.com/news/articles/2022-03-29/dallas-fed-sees-signs-a-housing-bubble-is-brewing-in-the-u-s |