Americans locked into lower mortgage rates have been increasingly unwilling to sell their homes.

Anonymous

You haven't even come close to doing all the math in support of your argument. And I mean all the math... and for a range of future scenarios. Take the most likely... that home prices stagnate nominally for the next five years. Start with that. |

Anonymous

It’s got to be across the board . The only viable politically |

Anonymous

And I guarantee it'll never happen. Too many politicians want to be reelected. It'll take 5 seconds for someone to come out... "I can't believe they want to cut the budget for x program for old/poor/education/military etc. How dare they!" |

Anonymous

And there in lies the problem. If that's your base case... No need to do any more math. |

Anonymous

You really don't understand how (and why) the Fed works, do you? |

Anonymous

Show me the breakeven. Do it. For a $1M house. How much does the value have to fall to break even? |

Anonymous

I don't even have to do the math. Whatever your net is going to be on a $1M house (could be $1M), you could rent a very nice home for $4K/mo (after paying tax on the interest income) without touching your principal and zero carrying costs. Wait for the market to normalize and buy again, if you want. For the foreseeable future interest rates will NOT go down (they can't), in fact they may go up even more. That makes cash even more valuable. Again, home prices are set at the margin. You don't want to be at the end of the line to sell, you wanna be at the front. |

Anonymous

|

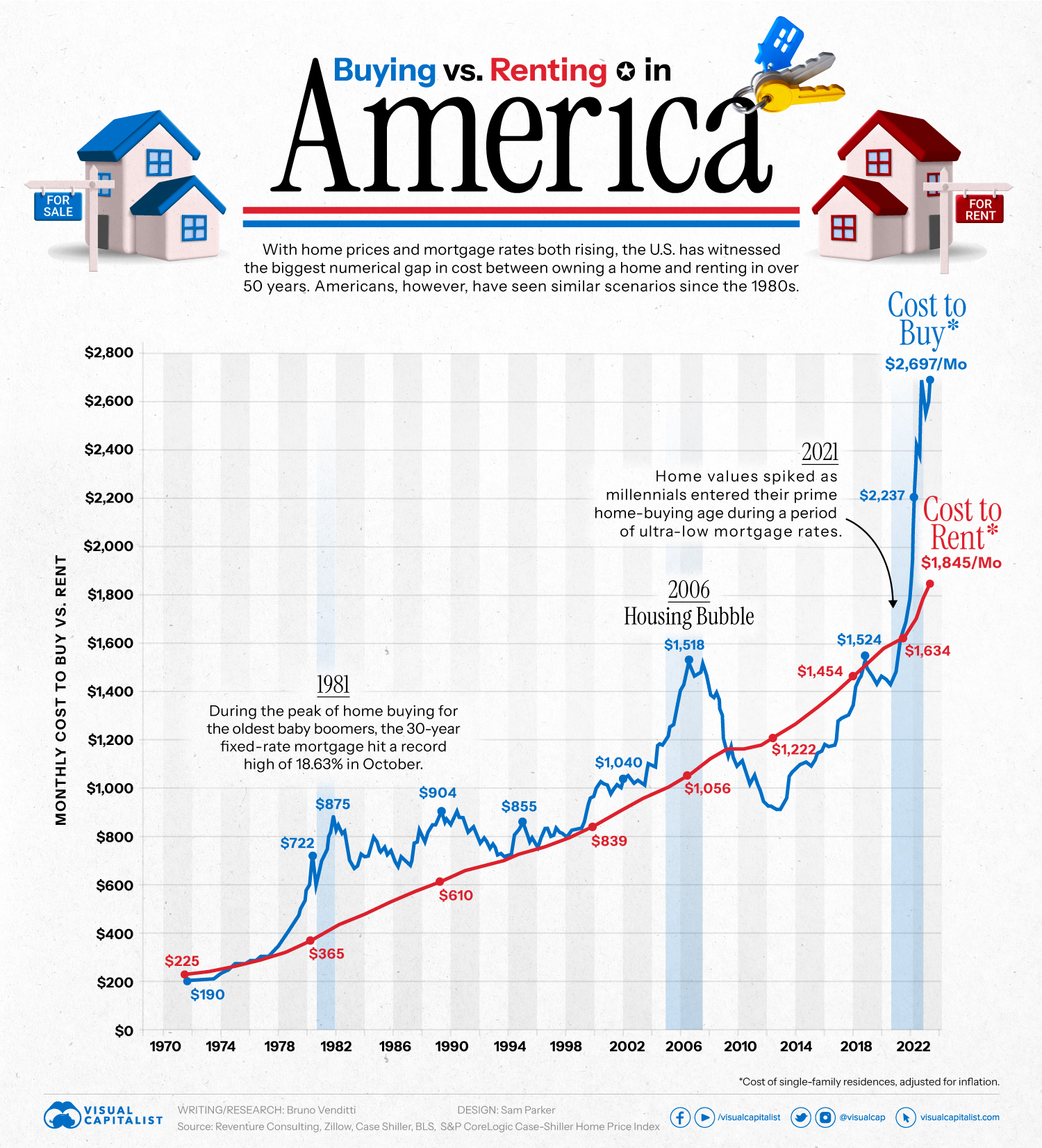

Here's a visual as to why the market is so out of whack. I'm sure you guys have seen this (or similar), and if you're a current homeowner (especially someone who bought during the last 3 years), it should make you nervous.

Trends are trends. They always go out of whack..and then normalize.

https://www.visualcapitalist.com/buying-vs-renting-house-in-america/ |

Anonymous

Haha. You’re so full of it. Do the math. What sort of price decline do u need to make your gamble pay off? |

Anonymous

|

Anonymous

Well if interest rates ever drop, then that would bring the blue line down without necessarily a nominal drop in housing. Anyone who recently purchased could refi. And why can't rents continue to increase? Last I heard they were having bidding wars for rental properties as well. |

Anonymous

Full of...what? Common sense? Sure. I don't need to forecast a price decline, I can't. What I can see is the value of cash at present, as we speak. And home prices and cash are inversely related. If you can get a higher rate of return by holding cash (which has zero carrying costs) vs housing, which has pretty much the highest carrying cost and the most illiquid market, I'll always prefer cash. People have forgotten what holding cash looks like (through no fault of their own, the Fed's actions in the last decade and a half made it a non-viable option). |

Anonymous

|

Oh, and lemme add.

The ONLY thing and I mean the single biggest ONLY thing going/went for housing is leverage. Where else can you get 1:20 leverage for a normal person? Nowhere. But leverage works both ways. When it's going up, it's fantastic. When it's going down, your "investment"/money down is wiped out in a heartbeat and you're underwater. |

Anonymous

1m in cash yields around 2900/mo after tax. You'd still have to pay 1100/mo out of pocket to rent, which would probably be similar to carrying costs on the house. Hardly the deal of the century. |

Anonymous

I…I….I give up. You guys have your heads so far down in the sand… |