should I switch the fixed-income portion of my portfolio from munis to corporate and TIPS?

Anonymous

|

I'm a Wealthfront customer who follows their recommended diversification model; recently they've been pushing a new model.

For the 1/3 fixed income portion of the portfolio, which used to be invested all in ETFs tracking muni bonds, they are instead now recommending that I invest about 2/9 in an ETF tracking corporate bonds (with higher yield, but fully taxable) and 1/9 in TIPS (and divest from munis entirely). This is because I make too little money to benefit from the tax savings coming from munis, their model says (HHI < 300k). Is this a good idea? I supposed there are two questions here: - is corporate instead of muni a good idea now? - are TIPS a good idea? (I read that with inflation as it is they are poised to pay high interest, but I'm wondering if this isn't already priced in so it's too late now to buy them.) Also, this is not direct TIPS buying, it's via an ETF. Please don't comment on whether WF itself is a good idea or not. |

Anonymous

| I have done the math on munis in your bracket and they are dominated by equivalent treasury bonds in a high tax state (treasuries are state tax exempt). Buy tips if you want to hedge inflation. Corporates might actually be dominated by treasuries after tax depending on their yield and your tax situation. |

Anonymous

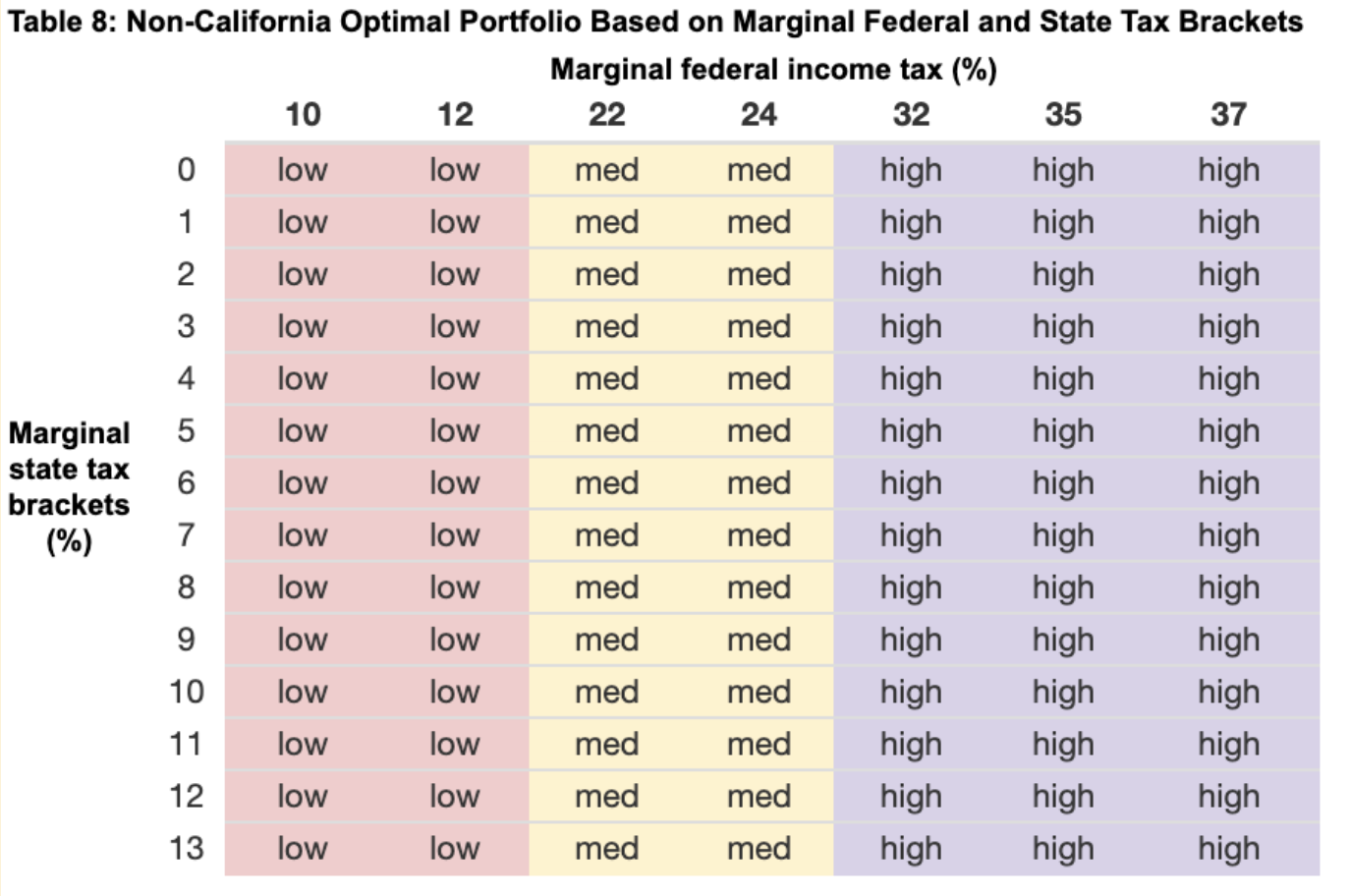

WF's math is published in their white paper. According to Table 8, I'm in the medium tax bracket (VA):

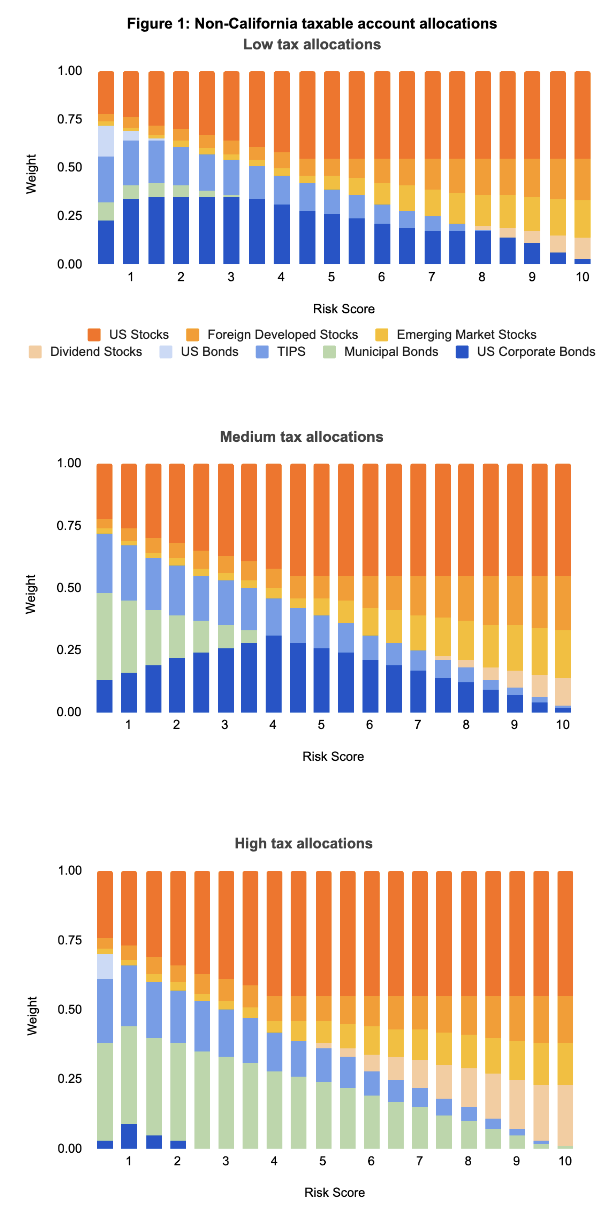

Then Figure 1 shows I shouldn't have munis unless I'm risk score 4 or lower (I chose 5).

My question is whether that makes sense. |

Anonymous

|

Of course it makes sense. Munis are only good for people facing higher marginal tax rates than you do at your income level.

TIPS have “priced in” expected inflation. But they are useful as a hedge against unexpected inflation. As for corporates vs treasuries, it depends on your risk profile. |