Anonymous

Anonymous wrote:Anonymous wrote:My mom has been 4 1/2 years in an assisted living facility. At the end of year 3, she ran out of money and LTC benefits, so we've been paying most of the bill since. (She has just social security income.) We pay about $5,500 a month baseline. When she needs extra care (she's fallen several times, for instance), we hire extra help by the hour, which gets expensive quickly. This month we spent closer to $9000. This is in a lower-cost-of-living state. We haven't moved her here because it would cost 50% more. Yes, we could apply for medicaid, but the decent places have long waiting lists, she's in a good place, and moving her would be challenging (she has dementia and high anxiety). So we suck it up.

What is your net worth and income? And your spouse is good with this? $5500-$9000 out of pocket per month is not feasible for most people, and even if it were, it would come at a huge trade-off and potentially cause marital problems. So, asking about your net worth and income because there is some number at which people can afford to help their parents at that rate without dooming themselves...

DP: if you cannot afford it, you simply don't do it. You apply for medicaid and let the chips fall where they do for your parents. You don't put yourself in massive debt/financial troubles to assist them.

But if you can you do. We paid the $500K+ entry fee for the CCRC for my parents. Simple, easiest way to provide care from a distance. It may cost us more (they are mid 80s and haven't gone beyond Ind Living yet), but all it will take is 2 years for each in advanced care and it will be worth it

Anonymous

Anonymous wrote:

OP - I think your approach to having the conversation with your parents about their financies and any LTC policies was spot on. Also to talk to them in dollar terms about the cost of future services. Folks say it is not your reponsibility, but the fact remains many adult children do step in to help aging parents. If the parents can't feel comfortable discussing finances or long terms aging issues directly with you, then do get the advice as mentioned of an Elder Attorney. This person might make the most sense in just reveiwing the legal instruments they have in place, especially in setting up the successive folks POA, Health Power on Decisions, Executor of the Estate etc. as needed. They will also have the experience in reading the fine details of contracts on LTC insurance policies and on any policies regarding future care as in a CCRC, Assisted Living or Memory Care residential program.

Other folks to have them speak with would be the place(s) that they are most likely to seek care support with either a local agency or an actual residential provider of services. Again this will be a time for both you and your aging parents to understand the services provided and the cost of such services. Every family is different in finances, dynamics and ability to face the future. You have done well to provide themw with housing close by you and how you proceed in the future should be governed by the needs of your children first of all, the financial health of your family (including your own future longterm care) and your own health. Parents are allowed to make unwise decisions, but you do not have to feel compelled topic up the pieces. We are the senior couple and we place the well-being of our adult daughters and their families as top priorities in legal and financial planning. I will say it is very surprising how fast a health issue can change the stability that an indepedent couple or single person has so keep the conversation going with your parents and with your spouse.

NP-Some older parents are absolutely unwilling to have these conversations, flat out refuse, will not meet with an attorney either. BTDT with our in-laws. Of course the more responsible people (like you) are the ones willing to discuss all this. People who bury their heads in the sand and are in bad shape are not more enclined to discuss finances as they get older. Right now in-laws are mid-70s and both working a lot, frankly because I doubt they'd make ends meet otherwise. So what happens next? It's very stressful to think about because as someone in this thread put very well "responsible children shoud not have to pay for irresponsible parents."

Anonymous

Anonymous wrote:Anonymous wrote:Medicaid only pays for skilled nursing care, not assisted living. I think it’s foolish, as skilled nursing care is much more expensive, but it is what it is.

No, Medicare only pays for skilled nursing care. Not assisted living, not long-term care in a nursing home. However, Medicare does cover home health care.

Medicaid covers long-term care in a nursing home. Generally does not cover care in assisted living.

Thank you for clarifying. It’s a confusing topic (not unlike SS). Some info to help round out the discussion, pulled from the two links below:

Assisted Living Statistics And Facts In 2025

“‘Overall, the supply of available beds in assisted living is greater than the demand,’ says Marcy Baskin, vice president of Senior Care Authority, an elder care consulting franchise headquartered in Petaluma, California. ‘However, that [balance] varies regionally, [and] we expect the supply-demand ratio to change as the baby boomer population ages.’

* Medicare doesn’t cover assisted living costs.

* Depending on the state Medicaid program, Medicaid may pay for assisted living services, and some also help cover room and board.

* A majority of assisted living residents use personal finances or long-term care insurance to cover assisted living costs.

How Many People Rely on Medicaid to Pay for Assisted Living?

* Nearly one in five (18%) of assisted living residents relies on Medicaid to pay for daily care services provided by assisted living communities.

* State Medicaid programs may pay for personal care and supportive services received in an assisted living community. However, Medicaid might not pay for room and board costs.

* A minority of state Medicaid programs don’t pay for services provided by assisted living communities.

* Depending on the state Medicaid program, following the death of a person in assisted living, their beneficiaries may be required to repay Medicaid for certain funds used to pay for their assisted living care and services in a process known as estate recovery.

‘Since assisted living is generally a private pay [industry], it’s typical for low- to middle-income families who don’t have long-term care insurance to lack the financial means to pay for assisted living, which creates a greater demand for Medicaid assistance,’ explains Baskin.

Medicaid is administered by each state, and each state’s regulations vary. ‘In some states, there are few options [available] for Medicaid covered assisted living costs, which forces someone needing care to move to a skilled nursing facility (which is more commonly covered by Medicaid),’ says Baskin.”

https://www.forbes.com/health/senior-living/assisted-living-statistics/

—

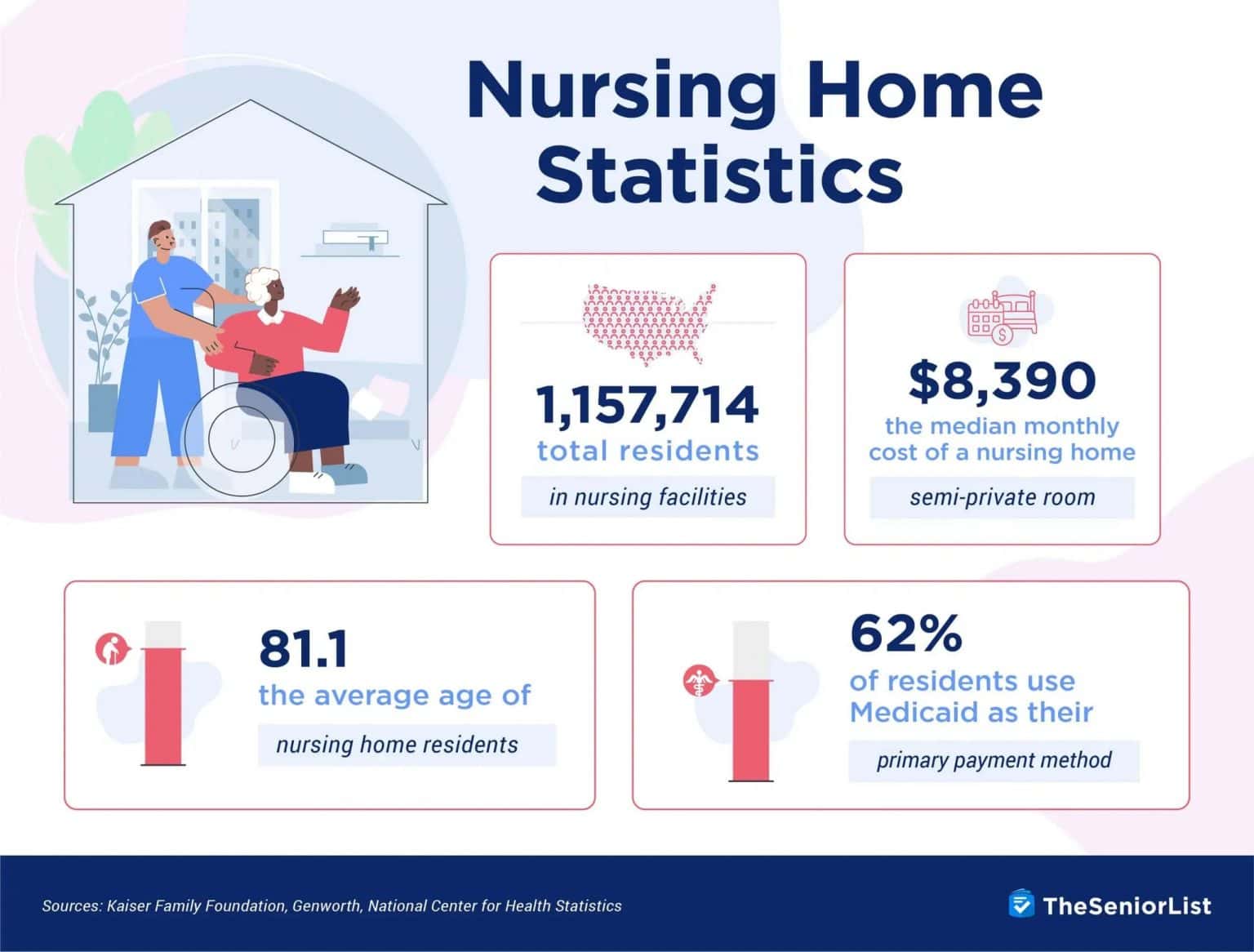

Nursing Home Statistics in 2025

”Nursing Home Residents

While the average length of long-term care is one year, 33 percent of today’s seniors are projected to require over two years of care.

Nursing Homes vs. Skilled Nursing Facilities

While the terms are often used interchangeably, nursing homes generally refer to facilities that offer permanent or long-term care, while skilled nursing facilities offer temporary care for residents while they undergo necessary rehabilitative treatment.

That said, stays in nursing homes can be temporary, and stays in skilled nursing facilities can last many days. That’s why Medicare will cover skilled nursing facility stays for up to 100 days.

Nursing Home Services

* 49.1 percent of nursing home residents require services related to Alzheimer’s or other forms of dementia.

Nursing Home Staff

* 54 percent of nursing homes turn away prospective residents due to staffing shortages

* Turnover rates for nursing homes are so high that data from the American Health Care Association and National Center for Assisted Living (AHCA/NCAL) predicts that they won’t return to pre-pandemic employment levels until 2027.”

https://www.theseniorlist.com/nursing-homes/statistics/

Anonymous

Anonymous wrote:Medicaid only pays for skilled nursing care, not assisted living. I think it’s foolish, as skilled nursing care is much more expensive, but it is what it is.

No, Medicare only pays for skilled nursing care. Not assisted living, not long-term care in a nursing home. However, Medicare does cover home health care.

Medicaid covers long-term care in a nursing home. Generally does not cover care in assisted living.