Anonymous

Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:It's pretty cringy when people throw around Cost of Attendance to exaggerate costs. Unless you're super rich you're not paying $85,000 a year for UChicago, nor are middle class people taking out "six figures" of loans for their child's undergrad. Most financial aid students at flagship state schools leave with $30k or so in loans. That's frankly not a big deal -- unless your kid flunks out. I believe the starting median salary for a bachelor's is now around $60k (?), so an average kid can easily pay off $30k in loans living at home for a year after graduation. Or even faster if they get an engineering degree or any other path that leads to a six-figure starting salary ex. nursing, tech, finance, or consulting.

There are such things as Parent Plus and private loans that allow you to take out more than that, and plenty families do.

Define plenty. I don't think it's that common for parents to take out loans, is it? For undergrad. When schools and College Scorecard report median loan sums of graduates, wouldn't the Parent Plus loans be factored in that as well? So the median is still about $30k for public U, right?

Looking at it, parent plus loan averages are about 30k and fed sub and unsub for public is 30k. Now the PP loans are split between private and public I guess, but I would say loans coming from school are reasonably higher than 30k

That's only federal data. Lots of parents borrow in other ways -- home equity loans, private student loans, borrowing from 401ks.

https://money.usnews.com/loans/student-loans/articles/parent-student-loan-borrowers-survey

Right. The actual cost of college is not just some 30k of student loans. PP scoffed at the idea of 100k in loans for public school. Students aren’t paying 60k in tuition and 20-30k in living expenses with 30k in student loans and their pt job at the dining hall.

+1 I was advising a student last year who got into VT. Very low income, qualified for Pell Grant. All he got in free aid was the Pell and the VA state grant, VT offered nothing else. He and his mom would have had to take out nearly $20k/year in loans, maybe a little less in later years if he could get cheaper off campus housing or work as an RA. I strongly advised that he not take on 100k in loans and consider CC first.

That is terrible advice. There is research showing poor kids who could go to VT tier university and instead go to CC tend to actually REGRESS and bomb out. I would have them call VT and explain the situation and of that fails, maybe drop down a rung to a university that offers more merit.

Anonymous

Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:It's pretty cringy when people throw around Cost of Attendance to exaggerate costs. Unless you're super rich you're not paying $85,000 a year for UChicago, nor are middle class people taking out "six figures" of loans for their child's undergrad. Most financial aid students at flagship state schools leave with $30k or so in loans. That's frankly not a big deal -- unless your kid flunks out. I believe the starting median salary for a bachelor's is now around $60k (?), so an average kid can easily pay off $30k in loans living at home for a year after graduation. Or even faster if they get an engineering degree or any other path that leads to a six-figure starting salary ex. nursing, tech, finance, or consulting.

There are such things as Parent Plus and private loans that allow you to take out more than that, and plenty families do.

Define plenty. I don't think it's that common for parents to take out loans, is it? For undergrad. When schools and College Scorecard report median loan sums of graduates, wouldn't the Parent Plus loans be factored in that as well? So the median is still about $30k for public U, right?

Looking at it, parent plus loan averages are about 30k and fed sub and unsub for public is 30k. Now the PP loans are split between private and public I guess, but I would say loans coming from school are reasonably higher than 30k

That's only federal data. Lots of parents borrow in other ways -- home equity loans, private student loans, borrowing from 401ks.

https://money.usnews.com/loans/student-loans/articles/parent-student-loan-borrowers-survey

Lol. That’s not “borrowing” anything. That’s called using ASSETS to pay for college. Truly poor people have no assets to pull large sums of money out of. It’s so funny to read how delusional upper middle class misers are. You’re such a victim and “indebted” because you took some equity out of your $750k-$2mn Arlington home. Lol.

Anonymous

Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:It's pretty cringy when people throw around Cost of Attendance to exaggerate costs. Unless you're super rich you're not paying $85,000 a year for UChicago, nor are middle class people taking out "six figures" of loans for their child's undergrad. Most financial aid students at flagship state schools leave with $30k or so in loans. That's frankly not a big deal -- unless your kid flunks out. I believe the starting median salary for a bachelor's is now around $60k (?), so an average kid can easily pay off $30k in loans living at home for a year after graduation. Or even faster if they get an engineering degree or any other path that leads to a six-figure starting salary ex. nursing, tech, finance, or consulting.

There are such things as Parent Plus and private loans that allow you to take out more than that, and plenty families do.

Define plenty. I don't think it's that common for parents to take out loans, is it? For undergrad. When schools and College Scorecard report median loan sums of graduates, wouldn't the Parent Plus loans be factored in that as well? So the median is still about $30k for public U, right?

Looking at it, parent plus loan averages are about 30k and fed sub and unsub for public is 30k. Now the PP loans are split between private and public I guess, but I would say loans coming from school are reasonably higher than 30k

That's only federal data. Lots of parents borrow in other ways -- home equity loans, private student loans, borrowing from 401ks.

https://money.usnews.com/loans/student-loans/articles/parent-student-loan-borrowers-survey

Right. The actual cost of college is not just some 30k of student loans. PP scoffed at the idea of 100k in loans for public school. Students aren’t paying 60k in tuition and 20-30k in living expenses with 30k in student loans and their pt job at the dining hall.

+1 I was advising a student last year who got into VT. Very low income, qualified for Pell Grant. All he got in free aid was the Pell and the VA state grant, VT offered nothing else. He and his mom would have had to take out nearly $20k/year in loans, maybe a little less in later years if he could get cheaper off campus housing or work as an RA. I strongly advised that he not take on 100k in loans and consider CC first.

Correction - $80k in loans (if he made it through in 4 years)

Anonymous

Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:It's pretty cringy when people throw around Cost of Attendance to exaggerate costs. Unless you're super rich you're not paying $85,000 a year for UChicago, nor are middle class people taking out "six figures" of loans for their child's undergrad. Most financial aid students at flagship state schools leave with $30k or so in loans. That's frankly not a big deal -- unless your kid flunks out. I believe the starting median salary for a bachelor's is now around $60k (?), so an average kid can easily pay off $30k in loans living at home for a year after graduation. Or even faster if they get an engineering degree or any other path that leads to a six-figure starting salary ex. nursing, tech, finance, or consulting.

There are such things as Parent Plus and private loans that allow you to take out more than that, and plenty families do.

Define plenty. I don't think it's that common for parents to take out loans, is it? For undergrad. When schools and College Scorecard report median loan sums of graduates, wouldn't the Parent Plus loans be factored in that as well? So the median is still about $30k for public U, right?

Looking at it, parent plus loan averages are about 30k and fed sub and unsub for public is 30k. Now the PP loans are split between private and public I guess, but I would say loans coming from school are reasonably higher than 30k

That's only federal data. Lots of parents borrow in other ways -- home equity loans, private student loans, borrowing from 401ks.

https://money.usnews.com/loans/student-loans/articles/parent-student-loan-borrowers-survey

Right. The actual cost of college is not just some 30k of student loans. PP scoffed at the idea of 100k in loans for public school. Students aren’t paying 60k in tuition and 20-30k in living expenses with 30k in student loans and their pt job at the dining hall.

+1 I was advising a student last year who got into VT. Very low income, qualified for Pell Grant. All he got in free aid was the Pell and the VA state grant, VT offered nothing else. He and his mom would have had to take out nearly $20k/year in loans, maybe a little less in later years if he could get cheaper off campus housing or work as an RA. I strongly advised that he not take on 100k in loans and consider CC first.

Anonymous

Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:It's pretty cringy when people throw around Cost of Attendance to exaggerate costs. Unless you're super rich you're not paying $85,000 a year for UChicago, nor are middle class people taking out "six figures" of loans for their child's undergrad. Most financial aid students at flagship state schools leave with $30k or so in loans. That's frankly not a big deal -- unless your kid flunks out. I believe the starting median salary for a bachelor's is now around $60k (?), so an average kid can easily pay off $30k in loans living at home for a year after graduation. Or even faster if they get an engineering degree or any other path that leads to a six-figure starting salary ex. nursing, tech, finance, or consulting.

There are such things as Parent Plus and private loans that allow you to take out more than that, and plenty families do.

Define plenty. I don't think it's that common for parents to take out loans, is it? For undergrad. When schools and College Scorecard report median loan sums of graduates, wouldn't the Parent Plus loans be factored in that as well? So the median is still about $30k for public U, right?

Looking at it, parent plus loan averages are about 30k and fed sub and unsub for public is 30k. Now the PP loans are split between private and public I guess, but I would say loans coming from school are reasonably higher than 30k

That's only federal data. Lots of parents borrow in other ways -- home equity loans, private student loans, borrowing from 401ks.

https://money.usnews.com/loans/student-loans/articles/parent-student-loan-borrowers-survey

Right. The actual cost of college is not just some 30k of student loans. PP scoffed at the idea of 100k in loans for public school. Students aren’t paying 60k in tuition and 20-30k in living expenses with 30k in student loans and their pt job at the dining hall.

Anonymous

Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:Tuition has exploded. Someone has to foot the bill.

https://tcf.org/content/report/parent-plus-borrowers-the-hidden-casualties-of-the-student-debt-crisis/

Or maybe universities need to cut costs by cutting services.

Guaranteed revenue streams give them incentive to create more and charge more. Limit the loans.

Stafford loans (no co-signer required) are limited to $27k TOTAL, not per year, for dependent students. Meaning, your typical single, childless, civilian traditional student who is done with college before age 24.

Private loans beyond that amount come from companies like Discover & Sallie Mae. I’m not confident any regulation would be passed anytime soon to stop that.

I do however think federal PPLs are predatory and need limits.

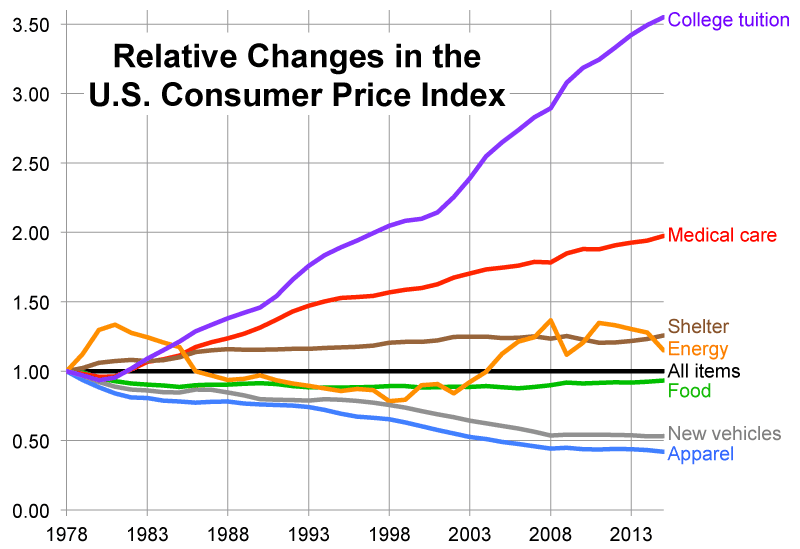

And tuition for VT is 60k for 4 years not including living expenses. That money has to come from somewhere and is. Tuition up 300%

Anonymous

Anonymous wrote:Anonymous wrote:I guess I disagree. An expensive but prestigious undergrad might cost more, but nobody can ever take degree away from you. You don’t know whether you’ll go to grad school or straight to work. I’d go for the best school you can get into.

They can't take away from you your dignity, your self-respect, or your sense of morality. I wouldn't exactly put a diploma on that level.

Are you insane? Those things can absolutely be taken away. What planet do you live on?

Anonymous

Anonymous wrote:Anonymous wrote:Anonymous wrote:Anonymous wrote:It's pretty cringy when people throw around Cost of Attendance to exaggerate costs. Unless you're super rich you're not paying $85,000 a year for UChicago, nor are middle class people taking out "six figures" of loans for their child's undergrad. Most financial aid students at flagship state schools leave with $30k or so in loans. That's frankly not a big deal -- unless your kid flunks out. I believe the starting median salary for a bachelor's is now around $60k (?), so an average kid can easily pay off $30k in loans living at home for a year after graduation. Or even faster if they get an engineering degree or any other path that leads to a six-figure starting salary ex. nursing, tech, finance, or consulting.

There are such things as Parent Plus and private loans that allow you to take out more than that, and plenty families do.

Define plenty. I don't think it's that common for parents to take out loans, is it? For undergrad. When schools and College Scorecard report median loan sums of graduates, wouldn't the Parent Plus loans be factored in that as well? So the median is still about $30k for public U, right?

Looking at it, parent plus loan averages are about 30k and fed sub and unsub for public is 30k. Now the PP loans are split between private and public I guess, but I would say loans coming from school are reasonably higher than 30k

That's only federal data. Lots of parents borrow in other ways -- home equity loans, private student loans, borrowing from 401ks.

https://money.usnews.com/loans/student-loans/articles/parent-student-loan-borrowers-survey

Anonymous

Anonymous wrote:Anonymous wrote:Anonymous wrote:Tuition has exploded. Someone has to foot the bill.

https://tcf.org/content/report/parent-plus-borrowers-the-hidden-casualties-of-the-student-debt-crisis/

Or maybe universities need to cut costs by cutting services.

Guaranteed revenue streams give them incentive to create more and charge more. Limit the loans.

Stafford loans (no co-signer required) are limited to $27k TOTAL, not per year, for dependent students. Meaning, your typical single, childless, civilian traditional student who is done with college before age 24.

Private loans beyond that amount come from companies like Discover & Sallie Mae. I’m not confident any regulation would be passed anytime soon to stop that.

I do however think federal PPLs are predatory and need limits.

Anonymous

Anonymous wrote:Anonymous wrote:Tuition has exploded. Someone has to foot the bill.

https://tcf.org/content/report/parent-plus-borrowers-the-hidden-casualties-of-the-student-debt-crisis/

Or maybe universities need to cut costs by cutting services.

Guaranteed revenue streams give them incentive to create more and charge more. Limit the loans.

Anonymous

Anonymous wrote:Tuition has exploded. Someone has to foot the bill.

https://tcf.org/content/report/parent-plus-borrowers-the-hidden-casualties-of-the-student-debt-crisis/

Or maybe universities need to cut costs by cutting services.

Anonymous

Tuition has exploded. Someone has to foot the bill.

https://tcf.org/content/report/parent-plus-borrowers-the-hidden-casualties-of-the-student-debt-crisis/

https://tcf.org/content/report/parent-plus-borrowers-the-hidden-casualties-of-the-student-debt-crisis/

Anonymous

Anonymous wrote:Anonymous wrote:Anonymous wrote:It's pretty cringy when people throw around Cost of Attendance to exaggerate costs. Unless you're super rich you're not paying $85,000 a year for UChicago, nor are middle class people taking out "six figures" of loans for their child's undergrad. Most financial aid students at flagship state schools leave with $30k or so in loans. That's frankly not a big deal -- unless your kid flunks out. I believe the starting median salary for a bachelor's is now around $60k (?), so an average kid can easily pay off $30k in loans living at home for a year after graduation. Or even faster if they get an engineering degree or any other path that leads to a six-figure starting salary ex. nursing, tech, finance, or consulting.

There are such things as Parent Plus and private loans that allow you to take out more than that, and plenty families do.

Define plenty. I don't think it's that common for parents to take out loans, is it? For undergrad. When schools and College Scorecard report median loan sums of graduates, wouldn't the Parent Plus loans be factored in that as well? So the median is still about $30k for public U, right?

For NYU, USC, Pitt and Penn State, it is very common to take out thousands in PPLs or private loans. Pitt’s average student debt is $40k+

Anonymous

Anonymous wrote:Anonymous wrote:Anonymous wrote:It's pretty cringy when people throw around Cost of Attendance to exaggerate costs. Unless you're super rich you're not paying $85,000 a year for UChicago, nor are middle class people taking out "six figures" of loans for their child's undergrad. Most financial aid students at flagship state schools leave with $30k or so in loans. That's frankly not a big deal -- unless your kid flunks out. I believe the starting median salary for a bachelor's is now around $60k (?), so an average kid can easily pay off $30k in loans living at home for a year after graduation. Or even faster if they get an engineering degree or any other path that leads to a six-figure starting salary ex. nursing, tech, finance, or consulting.

There are such things as Parent Plus and private loans that allow you to take out more than that, and plenty families do.

Define plenty. I don't think it's that common for parents to take out loans, is it? For undergrad. When schools and College Scorecard report median loan sums of graduates, wouldn't the Parent Plus loans be factored in that as well? So the median is still about $30k for public U, right?

Looking at it, parent plus loan averages are about 30k and fed sub and unsub for public is 30k. Now the PP loans are split between private and public I guess, but I would say loans coming from school are reasonably higher than 30k

Anonymous

Anonymous wrote:Anonymous wrote:It's pretty cringy when people throw around Cost of Attendance to exaggerate costs. Unless you're super rich you're not paying $85,000 a year for UChicago, nor are middle class people taking out "six figures" of loans for their child's undergrad. Most financial aid students at flagship state schools leave with $30k or so in loans. That's frankly not a big deal -- unless your kid flunks out. I believe the starting median salary for a bachelor's is now around $60k (?), so an average kid can easily pay off $30k in loans living at home for a year after graduation. Or even faster if they get an engineering degree or any other path that leads to a six-figure starting salary ex. nursing, tech, finance, or consulting.

There are such things as Parent Plus and private loans that allow you to take out more than that, and plenty families do.

Define plenty. I don't think it's that common for parents to take out loans, is it? For undergrad. When schools and College Scorecard report median loan sums of graduates, wouldn't the Parent Plus loans be factored in that as well? So the median is still about $30k for public U, right?