Market crash in 2022?

Anonymous

| Anyone keeping dry powder to buy dips or are you minimizing cash holdings due to the high inflation? I’ve been doing the latter but am feeling nervous. I’m less than 2% in cash right now and been this way the past 18 months, everything else in index funds, real estate, crypto. |

Anonymous

Yes, I’m loading up on cash for this scenario by: i) aggressively paying down my mortgage, and ii) loading up on iBonds (I just set up a living trust to maximize the amount that I can purchase). If/when the crash happens, I’m going to use either a HELOC or a cash-out refinance to go into the market in a big way. And with the iBonds, obviously the money is tied up for 12 months but at least it eliminates the pain of holding cash. Sorry, but I’m just not buying into the market right now with valuations higher than they were the peak of the dot-com bubble. |

Anonymous

What do you mean maximize the amount you can buy? Beyond 10k limit? |

Anonymous

I bought $30,000 - $10,000 individually, $10,000 in my business and $10,000 in the new trust. |

Anonymous

And I’m going to do the same thing again in a couple of days now that it’s 2022. So that $60,000 of iBonds for one person in a matter of weeks. |

Anonymous

How are you coming to this conclusion? |

Anonymous

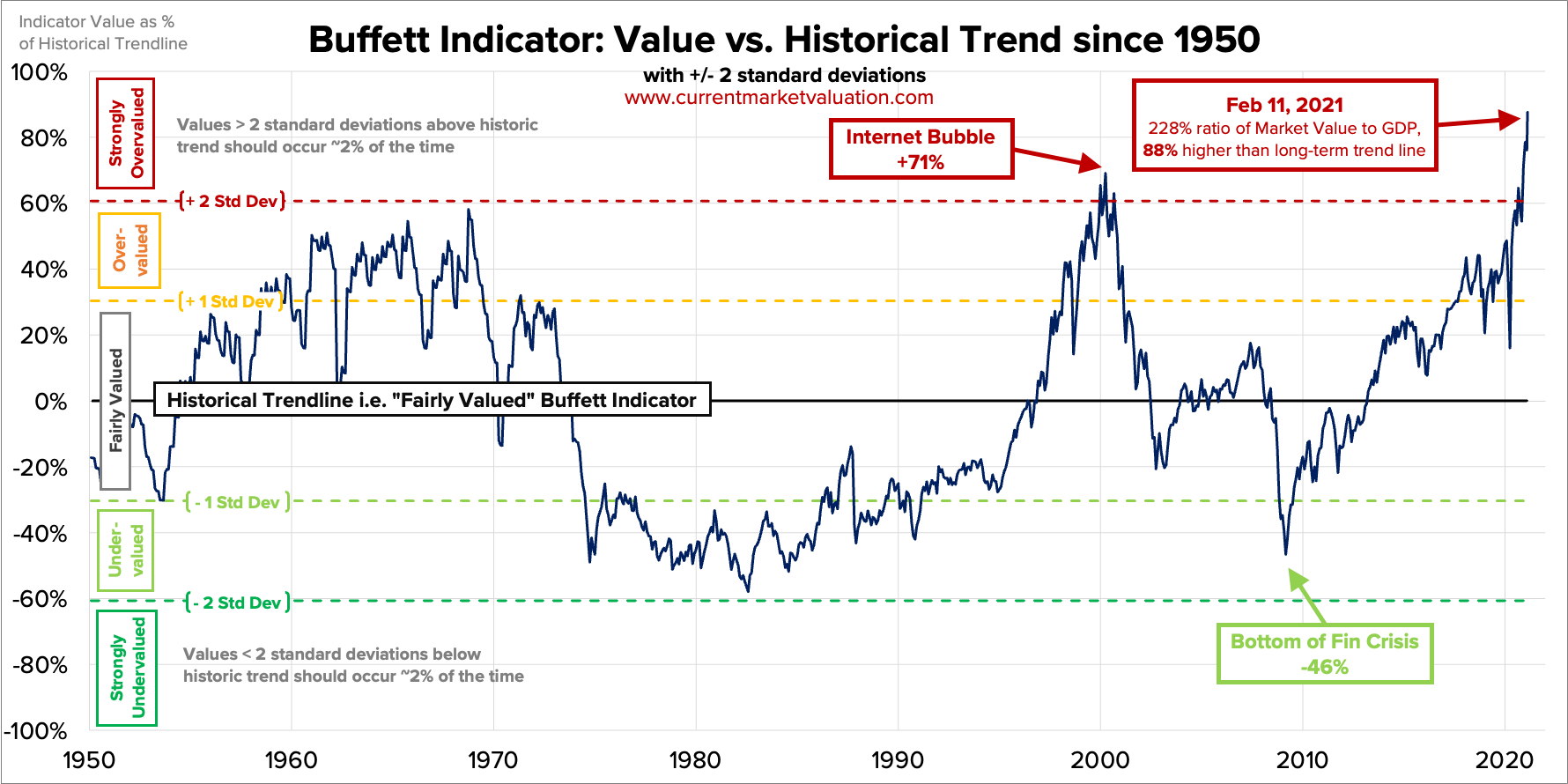

The Buffett Indicator, or the market cap of the total stock market compared to the GDP of the country, was made famous by Warren Buffett, who said it is the best measure of stock valuations. It is currently higher than in 2000 pre-crash, and this chart doesn't even fully capture the 27% increase in the S&P that took place in 2021.

|

Anonymous

Putting up a chart does not provide the necessary economic analysis for your conclusion. Try again. |

Anonymous

|

Sorry, but I’m just not buying into the market right now with valuations higher than they were the peak of the dot-com bubble.

How are you coming to this conclusion? The Buffett Indicator, or the market cap of the total stock market compared to the GDP of the country, was made famous by Warren Buffett, who said it is the best measure of stock valuations. It is currently higher than in 2000 pre-crash, and this chart doesn't even fully capture the 27% increase in the S&P that took place in 2021.

Putting up a chart does not provide the necessary economic analysis for your conclusion. Try again. Where can I find this analysis? Do you think stocks are fairly valued? |

Anonymous

|

Time in market beats timing the market.

Everybody thinks they know when to buy the dips, nobody actually does. Go play this game 100 times and let me know your scores, I bet you'll win far less than 50% of the time. https://www.personalfinanceclub.com/time-the-market-game/ |

Anonymous

| I'm going to continue to dollar cost average via paycheck contributions to my 401k and the kids' two plans, but I'm leaving this year's bonus in cash (other than $10k I already allocated to iBonds for 2022). Usually I invest my year-end bonus and quickly as I can, but this year I'm going to wait for a month and then maybe dollar cost average it into a brokerage account over the course of 2022. |

Anonymous

| Continuing to buy through 401k and DH's PSP. Keeping some cash for alternative investments should anything interesting come up. |

Anonymous

| If you follow the logic of the chart above you wound't have bought any equities since 2012. |

Anonymous

I plowed $600,000 into the market from Jan-April of 2021. As it went down, I kept buying. It required nerves of steel, but I did it. But, I agree with your point -- time in the market does beat timing the market. |

Anonymous

Lol @ nerve of steel. I clap you. |